Asteroom Editorial

Hybrid Appraisal ROI

One of the first hurdles for banks adopting hybrid appraisals is developing a business case and rationale that can be shared with executives in production, credit risk and operations.

Feb 18, 2026

What is the business case and ROI for hybrid appraisals?

There are three main reasons why banks are working now to transition to hybrid appraisals:

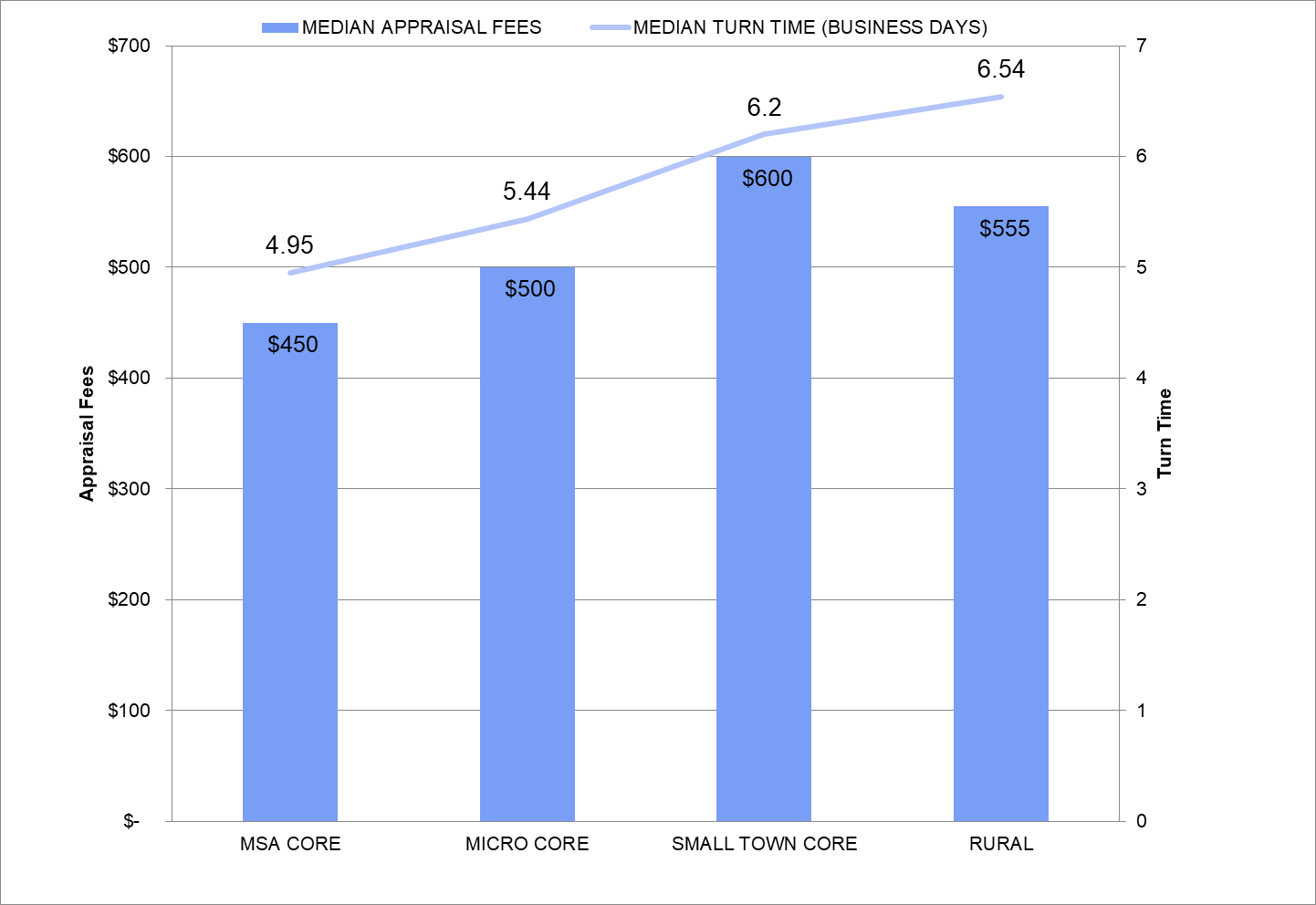

- Appraiser supply - In 2026, MtgeFi estimates there are ~37,000 active residential appraisers and Freddie Mac reports there are ~29,000 appraisers submitting to UCDP. In today’s higher rate environment, appraiser supply = demand.

- UAD 3.6 mandatory use - on November 2, 2026, the GSE will only accept appraisals submitted with the new Uniform Appraisal Dataset version 3.6, which requires appraisers to complete an appraisal using an entirely new process, which may lead to an imbalance of appraiser supply that can reliably perform UAD 3.6 appraisals.

- Refinance demand spikes - in 2016 and 2021 we experienced unforeseen refinance booms that resulted in extended appraisal turn times and higher fees

How hybrid appraisals mitigate these issues:

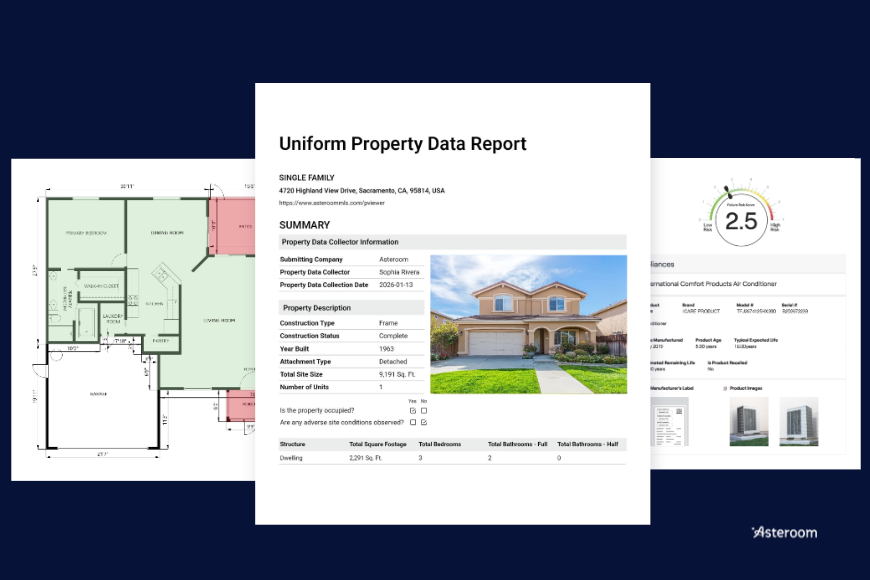

Following the appraisal supply issues in 2016, the FHFA and GSEs set about designing a standardized hybrid appraisal for agency use. The goal was simply to allow appraisers to complete appraisals without the need to visit the subject property. To facilitate this they designed a comprehensive property inspection, now known as a Uniform Property Data (UPD) report.

- Professional property data collectors complete inspections in 2-3 days - Asteroom uses state licensed real-estate brokers (1.5 million) - a huge professional workforce who are accomplished working with real-estate and borrowers.

- Appraisers can complete 3-5 hybrid appraisals per day - Asteroom provides appraisers the UPD and pre-populates the onsite inspection data, which is over 50% of the UAD 3.6 report.

Sign up Asteroom Newsletter

You might be interested in

隐私权和条款

>

Copyright © 2026 Asteroom, Inc. All rights reserved.